Ronald Mwangombe was one of the 85 members of the Ndara B Community who spent a full day evaluating the institution's town development plan, which has become the Diaspora University Town (DUT). He is happy that the community members made the right choice of embracing the building of a new town, university, and hospital. Today, DUT is at a point where Voi residents can join to tap Ksh 25 billion from KMRC, with 3,500 townhouses planned, each tapping about Ksh 7 million.

Kenya Mortgage Refinance Company was founded in 2019 and has since raised over Ksh 45 billion in capital and loans for financing residential mortgage loans. In the KMRC 2025 financial statement, the cash balance was reported at Ksh 17 billion. This showed the cash available for residential houses.

Ronald gives the following reasons to tap this money through the DUT 20,000 job creation and 3,500 townhouses plan:

1. Ksh 25 Billion Mortgage Money is Available.

KMRC was formed in 2019. The company would receive two credit lines from the World Bank and the African Development Bank totaling about KSh 40 billion. The amount withdrawn by the close of 2025 was Ksh 35 billion. Ksh 18 billion was used to fund mortgages in diverse counties, and Ksh 17 billion was held in cash and is available.

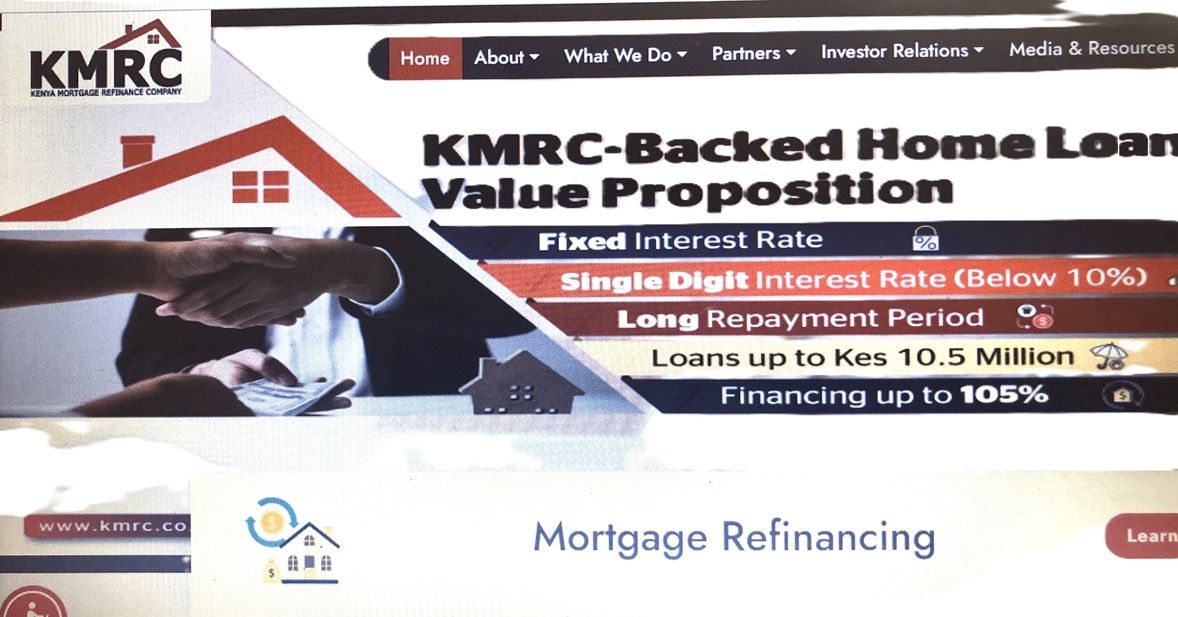

Another fact is that KMRC is set up to raise money as quickly as houses are built. The mortgage finance is today advanced by 34 financial institutions (14 banks and 20 SACCOs). The mortgage product: up to Ksh 10.5 million, 9% interest, 25 years.

2. Four (4) Banks Advancing the Mortgages are in Voi.

Of the 34 financial institutions listed as advancing KMRC mortgages, four banks have set up branches in Voi—namely, KCB Bank, DTB Bank, Absa Bank, and Cooperative Bank. Ronald is challenging the bankers in Voi to think outside the box so that this money can come to Voi and Taita Taveta.

3. Making new wealth using the Personal Unsecured Loan Products offered by Banks

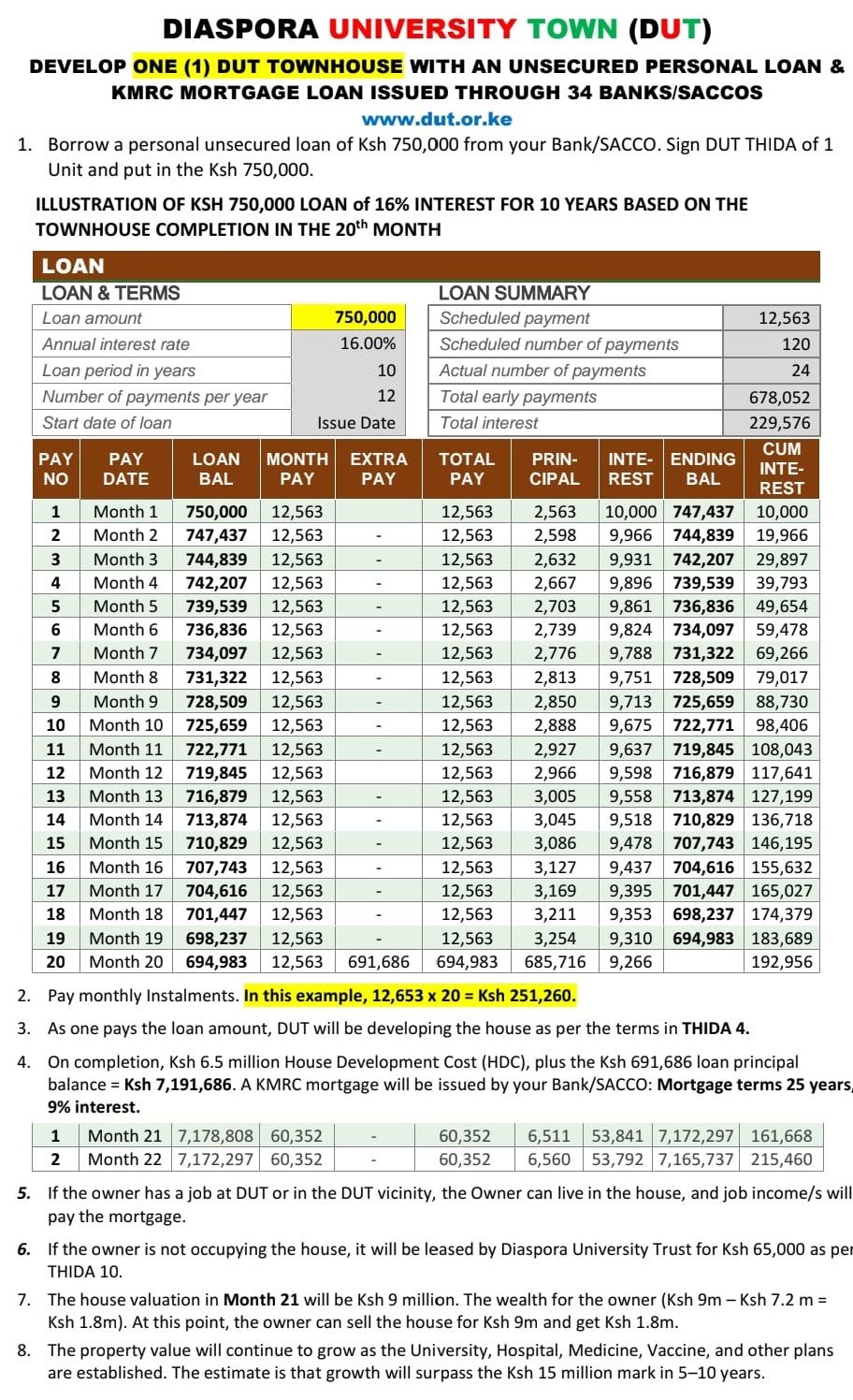

The personal unsecured loans offered by these banks will enable Voi residents to access money that they can apply as capital as they become DUT Townhouse developers. Government employees and others who qualify for the personal unsecured loan can take a 750,000 loan to capitalize the development of a townhouse and, in doing so, develop it by investing about Ksh 12,000–15,000 a month through loan payments. A townhouse will bring in Ksh 7 million in KMRC funds to Taita Taveta. The townhouse will increase the developers' wealth.

4. 20,000 Government Employees

Ronald challenges about 3% of the nearly 20,000 government employees in Taita Taveta County to tap into the unsecured loans offered by banks. The government employees include teachers, doctors, nurses, judicial members, police, national government departments, county government departments, and other government commissions. He gives the example of the KCB Bank loan product that reads, “Get a check off loan as a government employee, or a company that has an agreement with KCB Bank. The check-off loan of Kes 20,000 up to Kes 10 Million is repayable in up to 120 months (10 years), with monthly repayments remitted by your employer.” Similar products are available in other banks.

5. 20,000 Jobs Creation

When giving the reason of 20,000 jobs created, Ronald makes a plea on behalf of young people aged 25 and below, who will be the main beneficiaries. He asks those blessed with jobs and income to create these jobs by tapping KMRC funds.

6. Income for businesses

As the Ksh 25 billion flows to Taita Taveta, businesses will see a spike in revenue as the money enters the pockets of 20,000 workers who spend it in the Voi region.

7. Developing a New Town, University, and Hospital

Ronald says that one of the moments he felt he had done something important for himself, his family, his community, and future generations of Kenya was when he voted to grant the land the DUT project is now under development. He adds that those who join DUT will also feel proud to become founders of a new town, university, and hospital. When talking about the hospital, he says that, whether he is getting treatment, his grandchild is born, or any other medical event occurs, he will be happy to tell the story of how he and others helped build the hospital. He asks Voi residents to join so they can tell the story too.

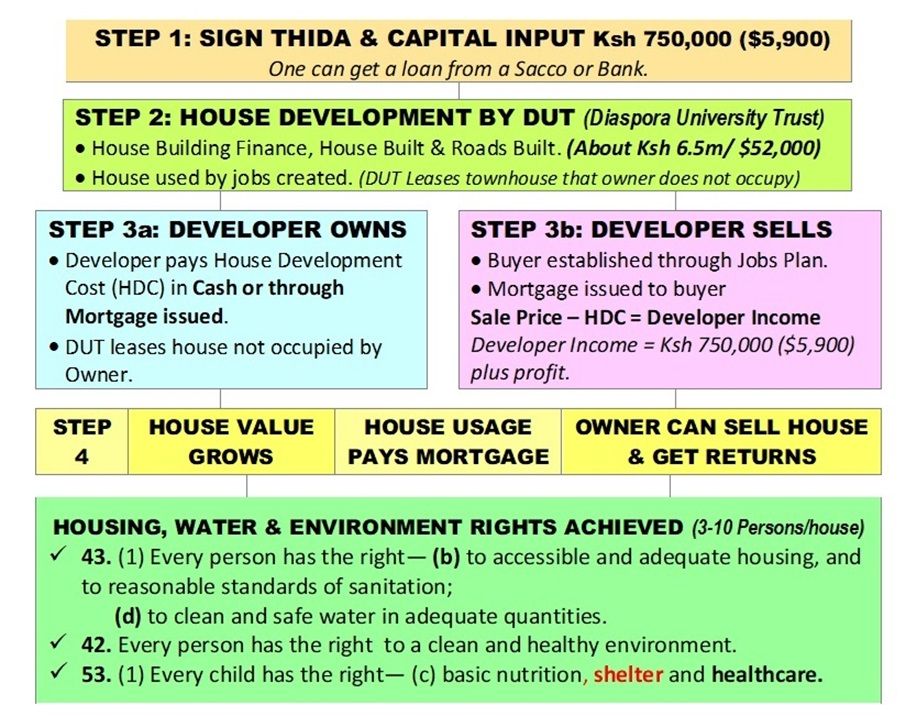

STEP BY STEP PROCESS OF DEVELOPING A DUT TOWNHOUSE WITH KSH 15,000

STEP 1. KSH 750,000

Visit a bank and borrow Ksh 750,000 through the bank's Personal Unsecured Loan products. Some of the Bank products that will make the loan repayment below Ksh 15,000 a month are:

KCB Bank Personal Unsecured Check-Off Loan

https://ke.kcbgroup.com/for-you/get-a-loan/unsecured-loan/check-off

Get a check-off loan as a government employee, or a company that has an agreement with KCB Bank. The check-off loan of Kes 20,000 up to Kes 10 Million is repayable in up to 120 months (10 years), with monthly repayments remitted by your employer.

Coop Bank Personal Unsecured Check-off Loan

https://www.co-opbank.co.ke/borrow/personal-loan/

Minimum loan amount of Ksh 50,000. Maximum loan amount: KES 10,000,000. Maximum term of up to 132 months (11 years)

DTB Bank Personal Unsecured Loan

https://dtbk.dtbafrica.com/account/unsecured-loan

Check off Non-Check loan, unsecured loan. Minimum Kes 50,000 up to Kes 6 Million. Tenor 96 months (8 years).

ABSA Bank Personal Unsecured Loan

https://www.absabank.co.ke/personal/get-a-personal-loan/#personalloancalculator

Borrow up to KES6,000,000 with no collateral required as security. Flexible repayment options up to 96 months

Monthly Payments of Loans based on 16% Interest

Based on a 16% interest rate, the monthly payments for the maximum loan period would be: Co-op Bank, Ksh 12,107; KCB Bank, Ksh 12,563; DTB, Ksh 13,897; and ABSA, Ksh 13,897.

Note that the bank's interest rate would determine the actual amount.

STEP 2. DUT-THIDA

Sign a DUT Townhouse Investment and Development Agreement (THIDA) https://dut.or.ke/THIDA2025.pdf and put the Ksh 750,000 in the Diaspora University Trust account.

At this point, a DUT townhouse developer file will be open and will start developing one townhouse.

STEP 3. PAY INSTALLMENTS AS THE DUT DEVELOPS THE TOWNHOUSE

Pay the monthly installments to your bank.

DUT, on the other hand, will develop the townhouse in accordance with THIDA Article 4.

In about 12–48 months, the DUT Design-Build plan will complete the townhouse.

STEP 4. COMPLETED HOUSE MORTGAGE

Upon completion of the house, get a KMRC mortgage through your bank.

The mortgage at this point can include the Principal Balance of the unsecured loan (Step 1), and the House Development Cost (THIDA Article 4).

The table in step 1 illustrates how the principal balance is incorporated into a mortgage.

STEP 5. COMPLETED HOUSE USAGE

The owner can occupy their house and live in a well-planned town with a clean and healthy environment, a University, a level 5/6 university hospital, good basic education schools for children, and other amenities.

If the owner does not live in the house, the owner can lease the house to DUT in accordance with THIDA Article 12 and receive Ksh 65,000 a month.

STEP 6. COMPLETED HOUSE EQUITY

Upon completion, each house will have equity calculated as Sale Price less the mortgage value. The sale prices are recorded in the DUT THD page https://dut.or.ke/thd

- Year 1 Sale Price. Ksh 8 million

- Year 2 Sale Price Ksh 8.5 million

- Year 3 Sale Price Ksh 9 million

- Year 4 Sale Price Ksh 9.5 million

- Year 5 onward Market Price.

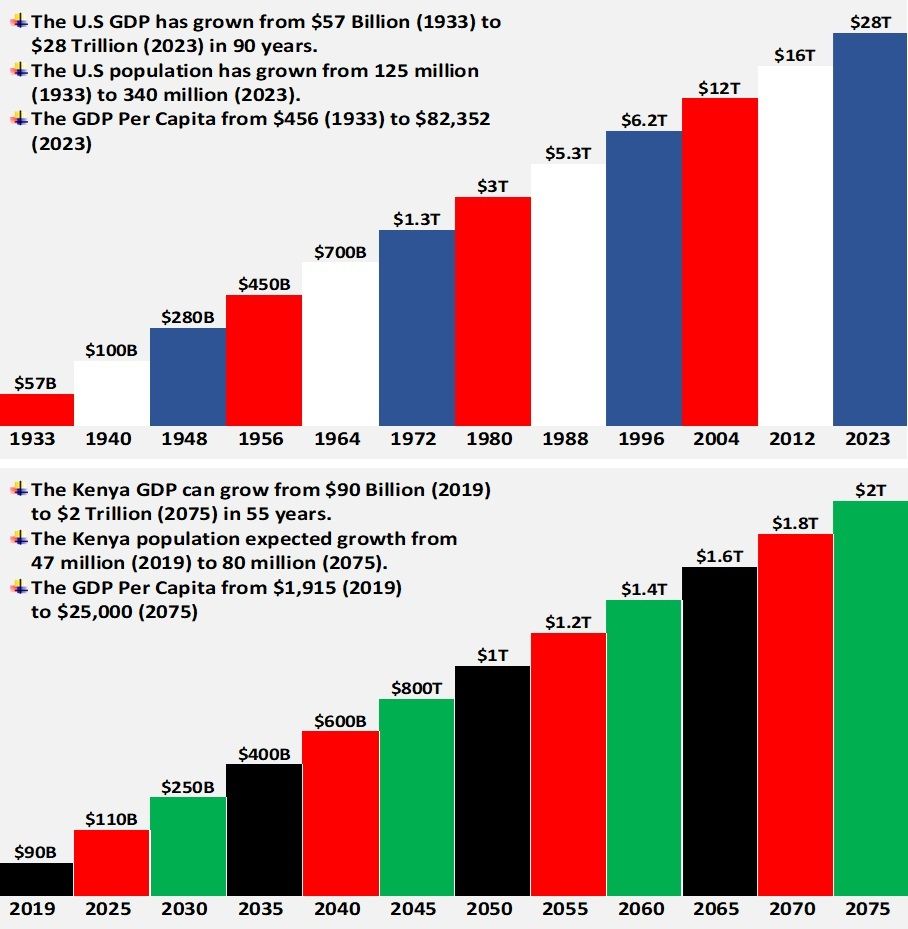

GDP GROWTH APPROACH

DUT uses the GDP Growth approach, which has grown the U.S. economy from $57 billion to the current $30 trillion. DUT will achieve a GDP of Ksh 20 billion.